The Silicon Valley Bank Collapse: A Failure Turned Into A Lesson

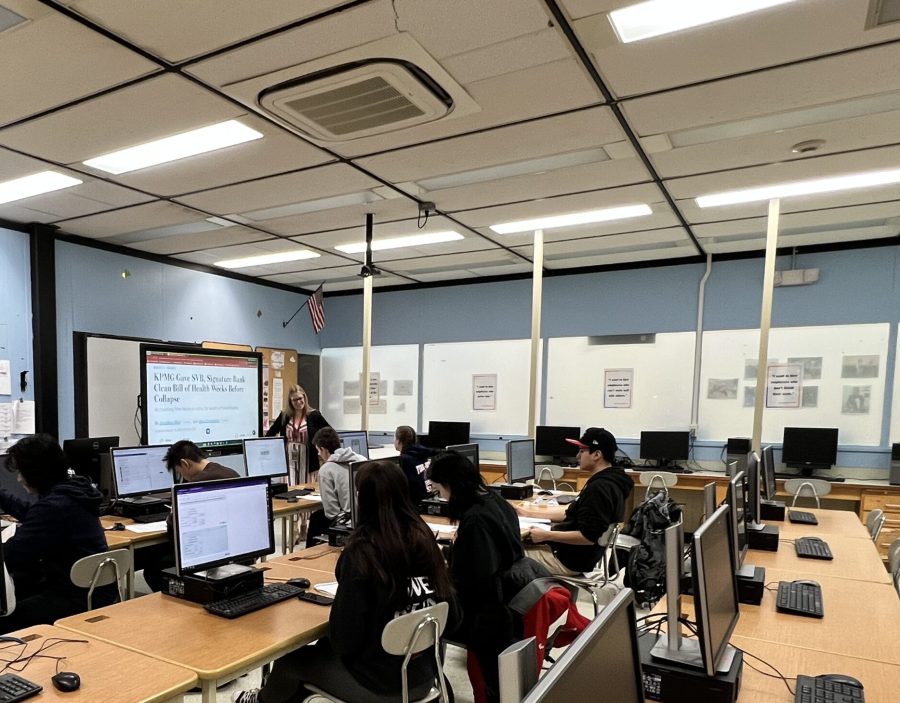

Ms. Geyer’s Accounting class sits in on a lesson about the collapse of SVB, and Signature Bank.

Throughout the world of education, teachers use real-world applications to broaden the horizons of the classroom and expand the knowledge of students. Rather than simply using a book or textbook, using real-world applications can engage students and show them the importance of the class itself outside of the actual classroom. Business classes throughout Lakeland Regional High School jumped on the opportunity to do just this with the recent collapse and sale of some big banks: Silicon Valley Bank (SVB), Signature Bank, and First Republic Bank.

Business teachers, Ms. Jessica Geyer and Mr. Gregg White, brought these current events into their accounting, personal fInance, and economics classes. They used the information from this huge news event and connected it to what they were presently teaching in class, showing students how they can use the news to be smarter with their money.

When interviewed by the Lancer Ledger on the lessons, Ms. Geyer said, “[My students] now… have a strong foundation on how to evaluate business transactions.” Ms. Geyer shared that she had her class start following the collapse of SVB and Signature Bank using news clips and Youtube. They also analyzed the bank’s balance sheets and found a “concerning level of long-term securities.” Ms. Geyer continued, “[The class] discussed the need for FDIC Insurance for banking consumers, and concerns of Long Term Debt posing Liquidity Issues for Firms, especially those in the financial sector. Banks need strong cash flow and liquidity to survive, and much of those resources were “tied up” for those two banks which ultimately led to their downfall.”

Additionally, when interviewed by the Lancer Ledger, Mr. White said, “In Economics we talk about reserve requirements (the amount of each bank deposit the bank must keep in the vault). We also talk about the relationship in the value of government bonds being – as interest rates go up – the value of a bond with a lower interest rate goes down.” Based on what is happening within the banks, the class learned the best time to buy long-term government bonds and how interest rates affect them.

Students were able to use their prior business knowledge learned in class to dive deeper into the cause of the bank’s collapse, and they were able to take these lessons to see how important it is to research a bank before investing sums of money in it and understanding of the right ways to invest.

The Ledger also got to find out more on the topic and what LRHS business students learned from these real world connections:

Junior Kate Rose explained her take on the failing of these banks: “In class, we’ve learned about Certificates of Deposit which are ways of investing money. CDs often have a high return percentage because banks need liquidity in order to run.” Not only did she use her prior knowledge to form connections, but she was also able to explain why banks sometimes fail: “Banks like the Silicon Valley bank failed because they did not have enough liquidity, or cash in their systems, to afford every customer the money that had been deposited into the bank.” March 10, 2023, the bank went bankrupt because of irresponsible donations, and the withdrawal of too much money from the small industries that had invested into it. The start up businesses played a part on the “run on the bank” after going on Twitter to talk about Silicon Valley’s liquidity concerns and its balance sheets. After hearing about these alaming details, more and more start up businesses withdrew their investments from the bank, which led to its complete bankruptcy.

When asked how banks protect depositors by the Ledger, senior Isabel Star explained, “Depositor insurance is what protects consumers from losing their money. This makes banking safe if you have under a certain amount of money in the bank.” She said she feels safe about investing money as long as it isn’t up in the millions.

Junior Nickolas Jusinski agreed and said, “[Insurance] makes banking safe, but you have to diversify where your money is to insure everything is safe. If your money is protected, it doesn’t matter too much if the bank crashes.”

Senior Benedict Nteko went more into depth about the topic and added, “Banks are heavily regulated by the government in order to ensure confidence in our financial system. Things like reserve requirements and FDIC insurance are safeguards to protect depositors.” Unlike the other two interviewees, he said even though this makes our banking and financial system relatively safe, there still are many unknowns that one cannot be prepared for.

In response to how the lessons learned in class will affect their banking decisions in the future, Jusinski said, “It makes you think about other banks potentially crashing, and connects to what we have learned about federally insured money in case something like this happened.” This shows how real-world applications have helped students like Jusinski think about bank safety and connect topics they have learned about earlier in class.

“It makes me think investing in banks can always be risky even if it’s a low risk investment.” junior Ilmi Kaba added.

Brianna is a sophomore at LRHS and this is her first year writing for The Lancer Ledger. She is excited to be taking Journalism 1 because it will help...

Rachel is a freshman at LRHS. This is her first year in journalism, and she is excited to start writing for The Lancer Ledger. Rachel is passionate about...

Erijona is a sophomore at Lakeland Regional High School. This is her first year writing for The Lancer Ledger, and she is very eager to start writing and...